When planning for homeownership, a common question arises: what percent of your salary should your mortgage be? Determining this percentage is crucial to ensure that your monthly mortgage payment is manageable, sustainable, and doesn’t strain your finances. Paying too much could limit savings, emergency funds, and lifestyle flexibility, while paying too little could restrict your ability to buy a home that meets your needs.

In this comprehensive guide, we’ll explore what percent of your salary should your mortgage be, examine financial rules of thumb, discuss influencing factors, provide examples, and answer frequently asked questions to help you make informed decisions about homeownership.

Understanding Mortgage Affordability

The first step in answering what percent of your salary should your mortgage be is understanding affordability. Mortgage payments typically include:

- Principal: The amount borrowed from the lender.

- Interest: The cost of borrowing.

- Taxes: Property taxes assessed by local governments.

- Insurance: Homeowners insurance protecting your home.

This combined monthly payment is often referred to as PITI. Affordability depends on how this total payment compares to your monthly income.

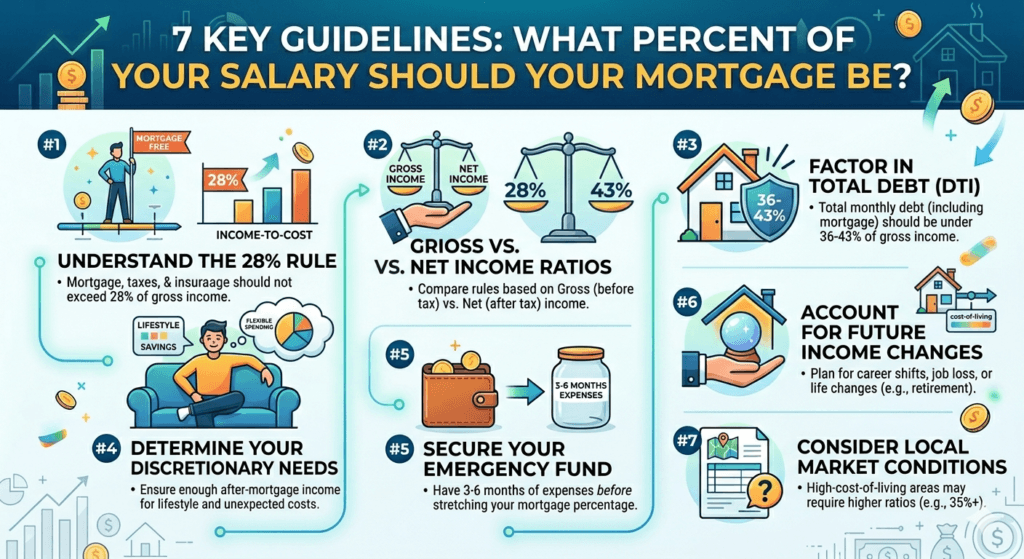

General Guidelines for Mortgage-to-Income Ratio

Financial experts suggest several approaches to determine what percent of your salary should your mortgage be:

| Rule of Thumb | Description | Percentage of Gross Income |

|---|---|---|

| 28% Rule | Monthly mortgage payment should not exceed 28% of gross income | 28% |

| 36% Rule | Total debt payments (mortgage + car + student loans) should not exceed 36% of gross income | 36% |

| 30% Rule | Conservative approach for total housing costs including taxes, insurance, HOA | 30% |

These guidelines provide a benchmark, but individual circumstances may require adjustments.

Factors That Influence Your Mortgage Percentage

Several personal and market factors determine what percent of your salary should your mortgage be:

- Income Level: Higher income may allow a slightly higher percentage without financial strain.

- Debt-to-Income Ratio: Lenders assess your total debts to ensure you can handle mortgage payments.

- Down Payment: Larger down payments reduce the principal and monthly mortgage payment.

- Interest Rates: Higher rates increase monthly payments, lowering the affordable mortgage percentage.

- Location: Property taxes, insurance, and home prices vary regionally, affecting affordability.

- Lifestyle and Expenses: Budget for emergencies, retirement, and discretionary spending.

Calculating Your Ideal Mortgage Payment

To calculate what percent of your salary should your mortgage be, follow these steps:

- Determine your gross monthly income.

- Apply the 28% rule (or your preferred ratio).

- Include estimated taxes and insurance to calculate total PITI.

- Adjust based on other debts and expenses.

Example:

| Annual Salary | 28% of Gross Monthly Income | Estimated PITI | Affordable Home Price |

|---|---|---|---|

| $80,000 | $1,867 | $2,000 | ~$350,000 |

| $100,000 | $2,333 | $2,500 | ~$450,000 |

| $120,000 | $2,800 | $3,000 | ~$550,000 |

Note: Assumes 30-year mortgage at 6% interest with 20% down payment.

How Down Payment Affects Mortgage Percentage

A larger down payment reduces your mortgage principal and can lower what percent of your salary should your mortgage be:

| Home Price | Down Payment | Loan Amount | Monthly Payment (P&I) |

|---|---|---|---|

| $400,000 | 10% ($40,000) | $360,000 | $2,160 |

| $400,000 | 20% ($80,000) | $320,000 | $1,920 |

| $400,000 | 30% ($120,000) | $280,000 | $1,680 |

By increasing your down payment, you reduce monthly payments and maintain a lower percentage of income toward your mortgage.

Mortgage Percentage and Budgeting Strategies

To determine what percent of your salary should your mortgage be, consider these budgeting strategies:

- Conservative Approach: Keep mortgage ≤25% of gross income to allow flexibility.

- Balanced Approach: Follow 28%–30% guideline for traditional affordability.

- Aggressive Approach: Stretch to 33%–35% only if debts are low and emergency savings are strong.

Additionally, consider building an emergency fund of 3–6 months of expenses before committing to a mortgage.

Examples Across Income Levels

Scenario 1: Entry-Level Income ($50,000/year)

| Rule | Monthly Mortgage Payment | Home Price Estimate |

|---|---|---|

| 28% Rule | $1,167 | ~$200,000 |

| 30% Rule | $1,250 | ~$210,000 |

Scenario 2: Mid-Level Income ($100,000/year)

| Rule | Monthly Mortgage Payment | Home Price Estimate |

|---|---|---|

| 28% Rule | $2,333 | ~$450,000 |

| 30% Rule | $2,500 | ~$480,000 |

Scenario 3: High-Level Income ($200,000/year)

| Rule | Monthly Mortgage Payment | Home Price Estimate |

|---|---|---|

| 28% Rule | $4,667 | ~$900,000 |

| 30% Rule | $5,000 | ~$950,000 |

These examples highlight how what percent of your salary should your mortgage be scales with income while staying within manageable debt limits.

FAQs on What Percent of Your Salary Should Your Mortgage Be

Q1: Is 30% of my salary too high for a mortgage?

A1: 30% is generally considered acceptable, but your total debts and lifestyle should be considered.

Q2: How does debt-to-income ratio affect mortgage affordability?

A2: A lower debt-to-income ratio allows you to allocate a higher percentage of income toward your mortgage safely.

Q3: Should I include taxes and insurance in the percentage calculation?

A3: Yes, including PITI provides a more accurate picture of affordability.

Q4: Can I exceed 30% if I have high income?

A4: Possibly, but ensure emergency funds, retirement, and discretionary spending are not compromised.

Q5: How does a larger down payment change the mortgage percentage?

A5: A higher down payment lowers principal, reducing the monthly payment and percentage of income spent.

Q6: Should I consider an adjustable-rate mortgage?

A6: ARMs can lower initial payments, but monthly payments may rise over time, affecting your salary percentage.

Q7: Is it better to stretch the mortgage limit or save more for a down payment?

A7: Saving more for a down payment usually lowers monthly payments and maintains a safer mortgage-to-income ratio.

Conclusion

Determining what percent of your salary should your mortgage be is a critical step in responsible homeownership. Following the 28%–30% rule, factoring in your down payment, interest rates, taxes, and insurance, and considering your overall financial situation helps ensure your mortgage is affordable and sustainable.

By carefully planning and using the examples and strategies provided, you can confidently select a home that fits your budget while maintaining financial health and flexibility. Whether you’re a first-time buyer or a seasoned homeowner, understanding the percentage of your income dedicated to mortgage payments empowers you to make smart and informed decisions.